Measuring Sustainability: Introducing ESG Benchmarks To Accelerate Sustainable Growth

As part of Revaia’s core values, we are committed to investing in and supporting our companies in their sustainability journeys. Placing environmental impact, diversity, and strong governance at the heart of a company’s mission benefits society broadly and the bottom line more specifically.

But as we spoke to our portfolio founders in recent months, we kept hearing a common refrain: There is a frustrating lack of comprehensive European ESG benchmarks for private companies taking into account the company’s maturity criteria (i.e. seed, series A…). This makes it difficult to set priorities and measure progress. And because those benchmarks that do exist are for mature public companies, it’s even harder for companies at different stages of development – from early stage to the very latest stages -- to truly gain the insight they need to evaluate their efforts.

We are firm believers that you can’t improve what you can’t measure.

So, to remedy this problem, we have developed the first European ESG Data Benchmark for startups which provides KPIs based on the maturity stage of tech companies. Through a survey of hundreds of companies conducted in partnership with The Galion Project and Bpifrance and with the support from Invest Europe, ImpactVC and 2CFinance, the report provides important baselines that we hope companies around the world will use to emulate best practices across the spectrum of ESG challenges.

Amid the myriad insights this work surfaced, there emerged one clear overarching message: ESG strategies and priorities must be adapted throughout all the stages of a company’s development. Being successful in this domain means remaining agile, vigilant, and honest about the impact of ESG programs as a company grows because making the right choices at the right time will optimize for success.

And let’s be clear about the stakes. The tech sector has a profound obligation to get this right. Tech companies are expected to be a major factor in job growth but at the same time their carbon emissions are on track to triple by 2050. They must be part of the solution and not the problem. But more than just not being bad actors, tech offers some of the greatest hope for solving social and environmental challenges through innovation and inclusiveness.

There is also a special burden for European Tech companies. Thanks to strong regulatory frameworks and forward-thinking founders, Europe and its startups stand as ESG beacons for the rest of the world. European entrepreneurs have led the way in developing innovative solutions to address these problems. Indeed, ESG represents a moment to demonstrate global leadership while also seizing a major business opportunity.

Inside the numbers

The survey at the heart of this report was conducted on an anonymous basis. The participants were evenly split across 5 stages, from Seed to Series D+. Startups from France accounted for a large majority of the response, not surprising because “Tech For Good” has been a pillar of the government’s economic development strategy.

What the data makes clear is that ESG projects should not be just checking a series of boxes. They must be embedded at the C-level and consistent with the values of the whole company. This is essential for avoiding a series of half-measures that fail to have the desired impact. For instance, a company might start a carbon footprint assessment but then not carry this all through the supply chain. Or it implements a diversity charter but doesn’t follow through on the plan when making routine hiring, promotion, and salary decisions. There is a risk of losing focus if it’s not systematically lived in the day-to-day process of the company.

If top executives are not on board then companies that seem committed as they are growing and on a great track will lose focus should problems or obstacles emerge in the business strategy. The team will inevitably backslide and ESG measures will likely be de-prioritized in favor of quick-fix measures.

A key strategy for success is appointing an ESG leader within the company (full-time or part-time). Our survey found that companies with an appointed ESG leader initiate on average 2.5 times more ESG projects than those without one. However, this presents its own risks if that leader leaves the company and projects languish. Even better is establishing an ESG team that can ensure continuity of efforts.

Among the three ESG categories, the study also found that startups seem to be prioritizing climate actions. Carbon footprint assessments and measuring Environmental footprint tend to be the first measures adopted, followed by engaging with suppliers to implement sustainable procurement charters. A focus on diversity then follows and eventually governance.

Let’s take a closer look at how a company’s level of maturity impacts three categories.

Environmental

If companies don’t implement a climate strategy early enough, they won’t truly understand where their emissions come from, which in turn will complicate de-carbonization efforts at later stages. Structural decisions such as choices about data centers will have been made that can be complex and costly to undo when a company is much larger, serving a big base of customers. If a company is late to climate strategy, it loses agility.

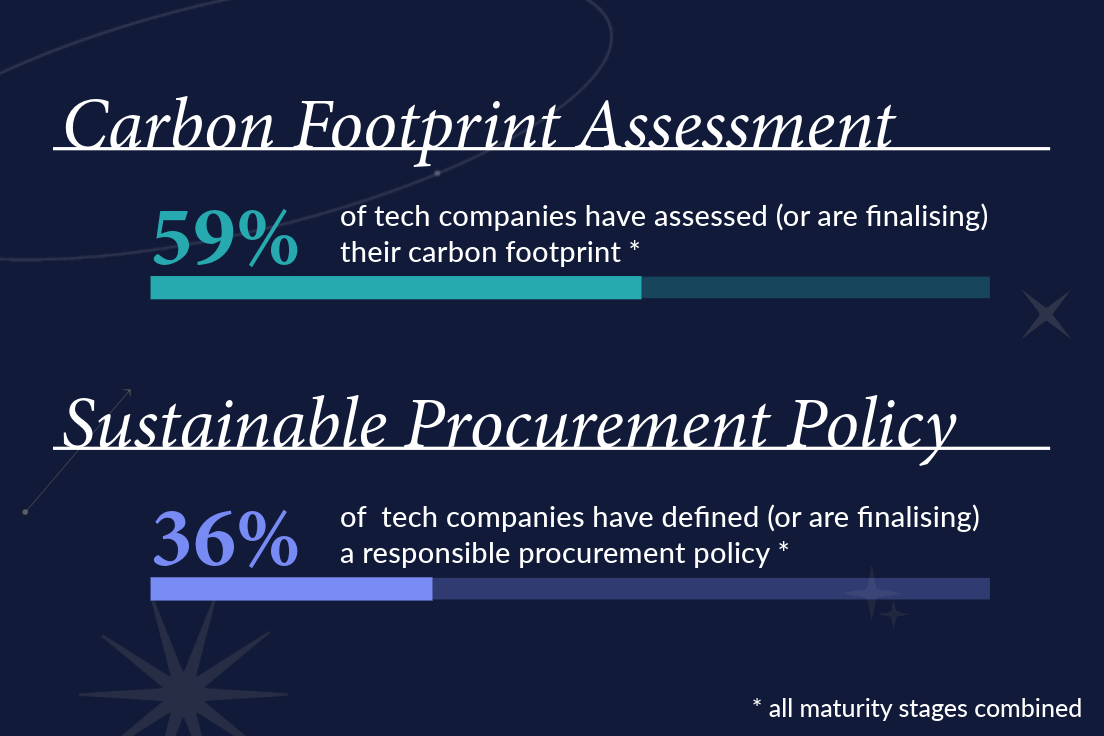

The survey found that when it comes to conducting a carbon footprint assessment, at the Series A about half of all startups has either performed or is finalizing this project, a ratio that rises to 87% at the Series D+ stage. There is also a high priority placed on formalizing an environmental policy, though that lags by about 10% across all stages compared to the carbon assessment.

For many companies, it may not make sense to assess the carbon footprint when they only have 10 employees. But it’s still important to identify this as an issue to be addressed so the company can continue to re-evaluate the feasibility, so they don’t miss the right moment to begin.

Before Series D+, less than 37% of companies have implemented a Responsible Procurement Policy. But by Series D+, 62% of companies have implemented one. Carbon compensation initiatives are less prevalent, with only 21% of companies putting this into practice by the Series D+ stage.

Diversity

This category also illustrates how the maturity of a company can impact its progress toward meeting ESG goals.

The study found that as a company matures and its board size grows, female representation decreases. While 37% of board members were female at the Seed stage, that fell to 27% by Series D+. Once they’ve ticked the box of having a female board member, companies seem to struggle increasing this ratio. (Governance in general also takes a hit: The presence of independent experts declined from 38% to 33% across those same stages.)

In addition, even when companies emphasize gender diversity, the tech teams plateaus at 21% female. To reach a gender diversity target of 50% in the workforce, companies focus on non-tech departments’ gender diversity ratio.

This highlights the challenge as companies become large. Leaders must ensure that everything they’ve implemented previously continues to be a key criteria when decisions are being made across the growth journey. And it’s here where the importance of an ESG leader can be especially important. For Series C and Series D+ companies without an ESG leader, the diversity ratio is only 38% compared to 46% when an ESG leader is appointed.

Governance

The topic of B Corp also varies across stages with early-stage companies being much more aggressive in their pursuit of this certification. While 23% of Series B companies have implemented a B Corp certification, only 18% of Series D+ companies have done so.

Obtaining this label becomes increasingly difficult as a company matures if it has not already implemented ESG measures much earlier in its history. Many older companies will shy away from this process because they believe they will fall short in too many measures, and the work to correct those flaws might feel too overwhelming or costly.

And yet, B Corp certification is becoming increasingly valuable because it demonstrates to internal and external stakeholders that a company is consistent in its policies and actions regarding sustainability and inclusiveness. We see younger employees being increasingly selective about choosing their employers based on such factors as their commitments to climate and diversity.

By understating where a company stands in relation to its peers in terms of ESG, we hope these benchmarks provide motivation to adopt the policies and make the investments needed to be leaders in their respective markets. Beyond that, these benchmarks should be a clear signal that investors are scrutinizing such criteria during the financing process as indicators of whether a company has the potential to be a champion.