Breaking Down Design & Creative Software Investment Opportunities

The Digital Creator Economy is projected to grow rapidly in the coming decade thanks to new technologies that democratize the ability to create content.

This phenomenon is disrupting a wide range of industries, creating immense opportunities for creators who are leveraging the vast array of tools and platforms that are emerging to express and communicate in ways that resonate strongly with audiences.

But while the size of the Creator Economy has become huge, it has been harder to fully understand from an investors’ point of view. At first glance, the market for Design & Creative tools that serve these creators is dominated by a few established giants such as Adobe as well as a couple of new breakout stars like Figma and Canva.

Indeed, VC investment in Design & Creative tools startups has been on a rollercoaster in recent years, currently at a low point that suggests that investors have soured on the potential. And yet, the number of Creator Economy participants continues to surge, and the tools to serve them are rapidly evolving.

So Revaia’s analysts have performed a deep dive into the Design & Creative tools market to better understand what’s driving this sector and how to think about where the value may be found for investors. As we continue to explore this market, we wanted to share our breakdown and thoughts on the underlying dynamics that are driving it.

The Big Picture

The size of the Creative & Design industry is exploding, a recognition of just how important expression and communication have become to just about every vertical in the digital age.

The global Creative & Design industry was valued at $2.1 trillion in 2021 and is projected to grow to $3.4 trillion by 2028. Within that sector, the Creative Software market is expected to grow to $13.4 billion from $8.5 billion over that same period.

What is catalyzing this growth? Broadly speaking, there are three categories of users: creative professionals such as architects, designers, artists, and content producers; communicators who need creativity and design to convey information, including students, marketers, knowledge workers, and businesses; and consumers who leverage this software for hobbies or building their social media identity.

The creative software market has expanded as these tools have trickled down from the estimated 49 million professionals to the 900 million communicators to the 5 billion consumers. Today, everybody can be a creator.

Source: Adobe Investor Meeting, Revaia Analysis.

Not surprisingly, these numbers drew the attention of VCs. In Q2 2021, Creator Economy companies in the U.S. raised $2.5 billion. By Q4 2023, that had fallen to about $100 million.

Of course, this drop is part of a global funding slowdown. But more specifically, there are some factors specific to Creative Software that explain its funding implosion – and why it remains complicated from an investor perspective.

While more consumers are joining the Creator Economy, only a few have managed to turn it into business. For instance, less than 5% of YouTube channels account for 90% of all subscribers. In addition, digital ad spending is falling.

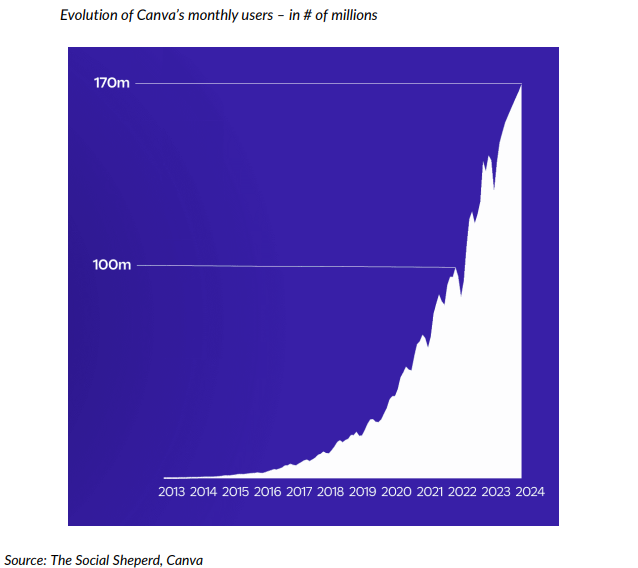

Finally, it’s a top-heavy market. Adobe, founded way back in 1982, looms large over the Creative Software industry, with a 49% market share. There has been room for other successes, such as Figma, founded in 2012, whose merger with Adobe was ultimately derailed by regulators. And Canva, founded in 2013, also has become a global success story.

But in general, the breakout stars that VCs want have been few. With the sector generating little in the way of exits, investors have become cautious.

The Case for Creative Software

Still, we think it’s a mistake to write off this market. Whatever the current position of the VC rollercoaster, the fact remains that the number of users is growing and adoption is accelerating. And in the process, it continues to transform the way people work across nearly all industries.

Among all categories of productivity software, design apps are some of the fastest-growing categories from a user perspective. As these tools become more accessible, they are being increasingly used by non-design teams which broadens the user base.

The combination of cost, ease of use, productivity, and collaboration led to 29% year-over-year growth among non-profits, 27% in government and energy sectors, 23% in logistics, 20% in entertainment, and 18% in education. Creative Software adoption is outpacing almost every other category of software – including HR, sales, security, and project management. The adoption across industries highlights the universal value of high-quality design.

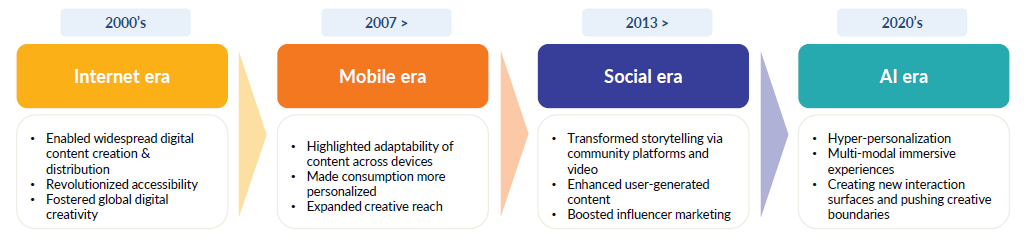

Platform shifts are also propelling this growth. We’ve seen the internet era turn into the mobile era and then the social era. Each shift has made this technology more accessible and created the need for content tailored to the way people interact with these platforms which enables increasingly personalized experiences.

Now we have moved into the AI era. New technologies such as GenAI make possible a new level of hyper customization and multimodal experiences. Creators are imagining new interactions at greater speeds and pushing creative boundaries along the way.

Source: Adobe Investor Meeting, Revaia Analysis

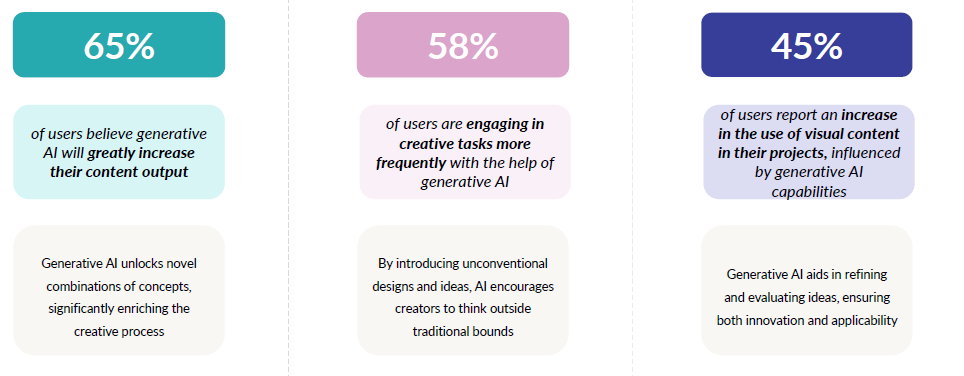

GenAI has already been a game changer as it automates content creation in just about any format – texts, images, videos, and even audio. Creators also believe that it improves content quality because it's quite often based on vast data sets. The potential to personalize content to specific targeted audiences represents a disruption that is in its very earliest stages.

While GenAI is getting much hype, it’s even more powerful when combined with other macro trends. Creators see AI as a powerful tool that augments human creativity and accelerates human creation, not just because of that automation.

It also enables a greater segmentation and specialization of tools that can be customized for the specific needs of different industries. New forms of collaboration have been unlocked, allowing more users to participate across an enterprise. These tools have given rise to passionate users who have created communities that further accelerate adoption. And finally, new platforms continue to arrive that hint at entirely new design demands – think Apple Pro Vision or the Metaverse.

Considering just a few decades ago the design industry existed almost entirely on paper, the extent of this digital revolution is remarkable.

A Creative Software framework

This brings us back to the question of how to think about this sector as investors. Even just defining what we mean by terms like “Creative Software” and “Creative Economy” can be tough given the pace of change and the way technology continues to evolve and blur traditional creative roles.

As we analyzed the market, we considered organizing it around formats (text, video, audio, visual), but that didn’t seem to define distinct categories for the tool makers. Eventually, we found it helpful to look at this market from the perspective of users and the creation lifecycle.

Even here, companies cross the defined categories. Creation is a messy process, no matter how sophisticated the tools are. Still, the lifecycle framework brought us to four categories that helped clarify our vision of the market:

- Thinking: This part of the process is all about research and conceptualization. Advanced analytics tools can be used to gain insights that shape product strategies, market understanding, and solution ideation. These tools facilitate more effective brainstorming by organizing ideas and enhancing collaborative efforts.

Examples: Pimento (GenAI platform that enables creatives to go from briefs into powerful creative directions); Murai (Visual collaboration platform intended to help cross-functional teams to brainstorm and ideate virtually); Mind Meister (Mind mapping tool that enables users to visualize, share, and present their thoughts mental maps).

- Creating: Creation moves fast and these tools enable the creative outputs in different formats by simplifying the production process which increases efficiency. The user experience makes it easier to align product design with market and brand identity.

Examples: Figma (Design tool intended to help build better products); Vistacreate (Online tool designed to easily create videos and graphic designs); Synthesia (AI technology for personalized and localized video content).

- Iterating: No creation is perfect the first time. So teams need to iterate and collaborate. A new generation of tools is making it easier to review designs, get feedback, and then enhance the concept. By streamlining the review and revision process, they facilitate real-time adjustments, ensuring projects remain aligned with strategic objectives and quality standards.

Examples: Adobe's Photoshop (online platform for photo editing); Jira (Project management tool for software teams to track issues and tasks); Canny (Customer feedback tool designed to help track user feedback to make better product decisions).

- Marketing: This includes deployment, monetization, and measurement. These tools ensure the project's market launch and financial viability. Digital marketing and social media tools are essential for successful project deployment and audience engagement. Analytics tools play a key role in refining monetization strategies and accurately measuring project performance against key metrics.

Examples: Patreon (Monetization platform that provides tools for content creators to run a subscription service and sell digital products); Jellysmack (Creative video platform for enhancing brand recognition and through social distribution); Etsy (E-commerce company focused on handmade or vintage items and craft supplies).

Revaia’s guidebook

We continue to study this market to see where emerging companies might align with our overall investment strategy. It remains a complex but exciting sector for several reasons: swings in valuations, the rapid evolution of technology, the mass adoption of design tools, and uncertainty around business models.

In assessing potential investment opportunities, we are guided by some of our standard investment guidelines:

- Look for user love. Communities are playing a big role in driving the adoption of these tools.

- Bet on the right team and stellar execution. Companies like Figma and Canva have seen success that has taken more than a decade to achieve. That’s impressive. But going forward, teams who want to compete with Adobe and other giants need to move fast. If you want to compete here, you need to be exceptional.

- Bootstrapped vs VC: Not every company is a VC play. Several interesting design companies have been around for decades and created sustainable businesses without outside investment. It’s important to understand how taking equity investments can create the kind of growth needed for investors.

- Be careful of the underlying tech. Some companies look impressive but are using old, legacy tech in their stack. This market is evolving super fast, so any company that needs to overhaul its infrastructure or relies heavily on outsourced human labor may not be nimble enough to adapt.

- Don’t be fooled by a company doing €5m of ARR. Though being an entrepreneur is never easy, the bar for a SaaS company to reach that level of recurring revenue is not that high, so not a great indicator of long-term traction. Investors have to be able to see whether this is a plateau or evidence of real product-market fit that will scale.

- Exits: All types of exits – M&A, PE, IPOs – are all challenged at the moment. And the collapse of the Adobe-Figma deals has cast a long shadow over exits for Design Software. At the same time, Adobe, Figma, and Canva all grew using savvy M&A to capture new markets and add new tools. So exits are tough, but truly disruptive tools will always be in demand by industry leaders looking to maintain an edge.

The bottom line: Design & Creative Tools is a surprisingly complex market, but one where the raw numbers indicate that disruption is accelerating and the technology is evolving. When there is massive disruption and massive adoption, there is likely to be an opportunity for investors who understand the underlying dynamics and where value is being created. Revaia remains optimistic about the transformational potential of this sector and we’ll be studying the ongoing shifts closely to find opportunities that can leverage our own experience and values.